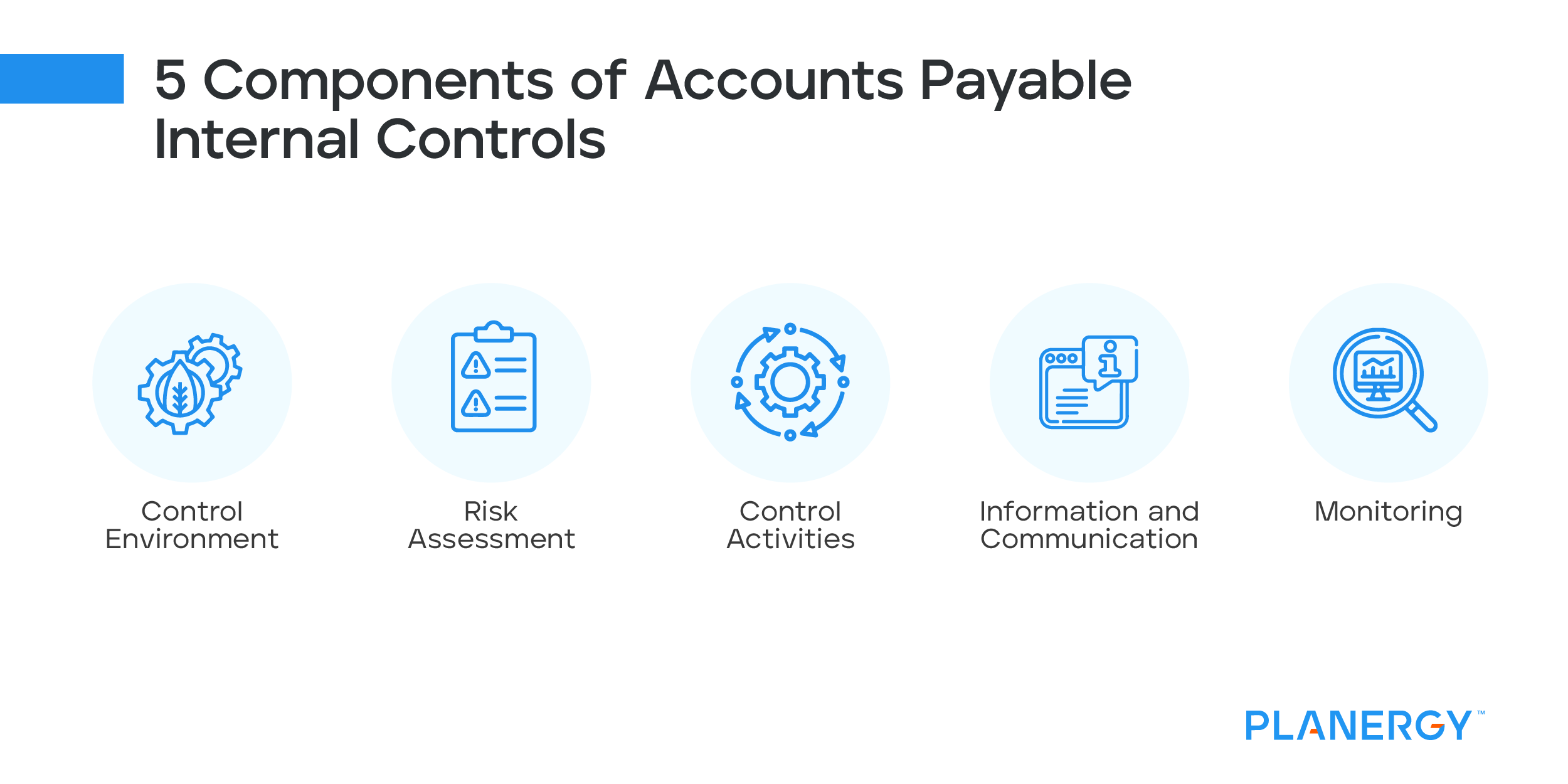

Once your business has established the appropriate internal controls across the accounting department, you need to delve a little further and establish AP internal controls to protect your monetary assets. AP controls include:

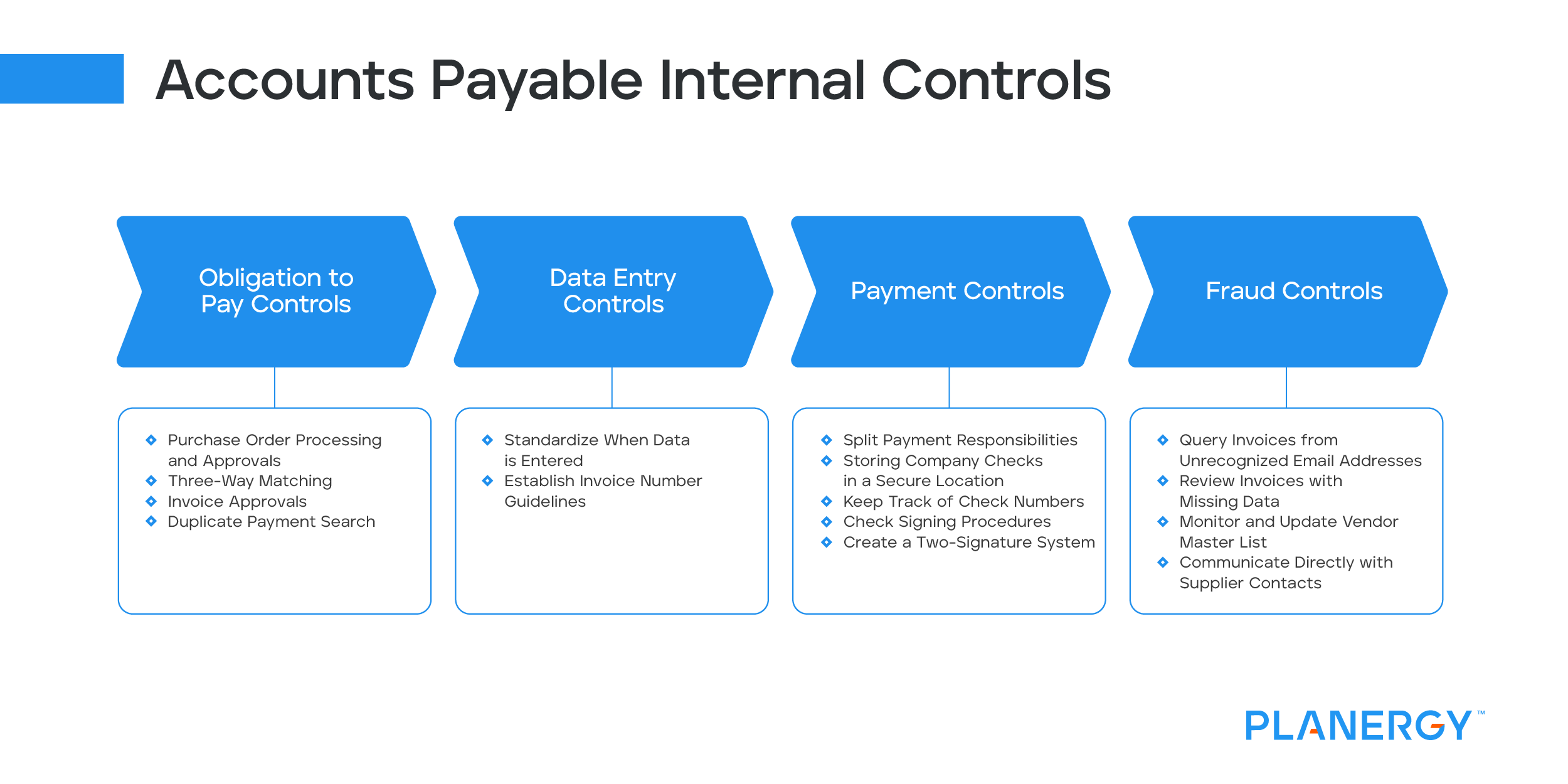

Obligation to pay controls cover four areas in the accounts payable process; purchase order approval, invoice approval, three-way matching, and duplicate payments. You’ll also need to have a payment approval process in place for invoices that do not require a purchase order.

-

Purchase Order Processing and Approvals

The procurement department should issue a purchase order for all approved purchases. This process approves all spending before an order is placed.

Because of this, the purchasing department should ask for a completed requisition prior to placing an order.

Since purchase orders require approval prior to an invoice being received, the invoice will not need to be routed to an approver before processing, provided that it matches the purchase order and shipping receipt.

-

Three-Way Matching

Even with an approved purchase order in hand, an AP clerk should still use the three-way match, which matches the purchase order, supplier invoice, and receiving documentation.

If your business is small and your paperwork is in order, this process is fairly straightforward, but larger businesses may find the process time-consuming.

This can be rectified by using AP automation, which will match all the required documents electronically, flagging you when something doesn’t match.

-

Invoice Approvals

For orders placed that do not require a purchase order, an invoice received from a vendor or supplier will need to be routed to an approver.

It may be better to route the invoice to the person who ordered the goods or services and then route it to a secondary approver so that two sets of eyes look at the invoice.

-

Duplicate Payment Search

Another reason to consider making the switch to AP automation is that the system will automatically search for duplicate payments.

Again, very small businesses will be able to complete this task manually, but if you commonly process hundreds of invoices monthly, the task can become overwhelming, particularly for a small AP staff.

Data entry controls ensure data entered in accounts payable has a standard process. This greatly reduces the risk of manual entry errors. Using AP automation software can greatly reduce the need for manual data entry but you should have controls in place as a fallback.

-

Standardize When Data is Entered

There are two ways to enter accounts payable invoices; as soon as they are received or after they have been approved.

If you currently have a purchase order system or a procure-to-pay software like Planergy, you can eliminate the need for invoice approval prior to entering the information, as all purchase orders should already be approved before the invoice is received.

If you don’t use a procure-to-pay system or the majority of your invoices are sent without a purchase order already created, it’s better to enter the invoice after it’s been approved.

Whatever process works for your business, it’s important that it’s clearly communicated to all staff members. Let’s look at the differences between these two approaches.

-

Enter Invoices Prior to Approval

If you’re using a purchase order system, entering vendor invoices prior to approval is fine, as the purchase order has already been approved. Invoices should not be entered before approval if a purchase has not been issued for the purchase.

-

Record After Approval

Any invoice received without a purchase order in place should be approved prior to entering it into your accounting application. In some cases, a vendor file may need to be reviewed prior to approving an invoice.

-

Establish Invoice Number Guidelines

One of the biggest causes of duplicate payments is not entering an invoice number as it’s shown on the invoice.

For example, an invoice is received and entered into the system with the number 000123. Three weeks later, a duplicate invoice is received, but this time, the AP clerk enters the invoice number as 123.

If a payment is processed for both invoices, the system will not flag it as a duplicate payment. Establishing guidelines for entering invoice numbers will help.

Along with the segregation of duties, which is mentioned earlier, there are other payment control measures that need to be properly managed, including the following:

-

Split Payment Responsibilities

Once an invoice has been approved for payment, one employee should be responsible for processing payments with a second employee approving the electronic payment, ACH transfer, or signing the check.

-

Store Company Checks in a Secure Location

The only people that should have access to company check stock are the employees responsible for processing payments. Check stock should always be stored in a secure location, along with any signature stamps, if they’re used.

Bank account numbers should also be restricted if electronic payments are utilized.

-

Keep Track of Check Numbers

Paying attention to check numbers is important, especially for those processing payments manually. It’s important that there is no gap in the check number sequence between the last check used for a previous check run and the first check to be used for the current payment cycle.

If you’re using an automated accounting system, it will track check numbers automatically, but be careful if the system allows you to override the check number sequence.

-

Check Signing Procedures

While it’s recommended that all checks should be signed manually, this may not be practical for very large businesses. If that’s the case, making the transition to an automated AP application may be the best solution, which eliminates the need to use checks in most if not all situations.

-

Create a Two-Signature System

For checks over a certain amount, consider adding an additional safeguard such as requiring two signatures. Again, having a second set of eyes on a check may discourage theft or fraudulent activities from occurring.

External fraud also needs to be monitored for, here are a few additional checks to help identify supplier procurement fraud: