There are three types of trial balances that are typically run, with each one building off of the other.

Unadjusted Trial Balance

The unadjusted trial balance is the first trial balance you’ll run, which includes the ending balances of all of your general ledger accounts before any adjustments have been made.

The unadjusted trial balance is an excellent starting point for reviewing ending balances and determining what adjustments need to be made.

Below is an example of an unadjusted trial balance for the period ending June 30, 2023.

| Account Number | Account Name | Debit | Credit |

|---|

| 1000 | Checking Account | $125,200 | |

| 1005 | Accounts Receivable | $27,000 | |

| 1020 | Inventory | $6,000 | |

| 2000 | Accounts Payable | | $15,450 |

| 2005 | Notes Payable | | $51,000 |

| 3000 | Stock | | $45,000 |

| 4000 | Revenue | | $57,000 |

| 5000 | Wages | $8,000 | |

| 5005 | Postage Expense | $1,500 | |

| 5020 | Insurance Expense | $750 | |

| | | | |

| | Totals | $168,450 | $168,450 |

The unadjusted trial balance reflects ending account balances before any adjusting entries have been posted.

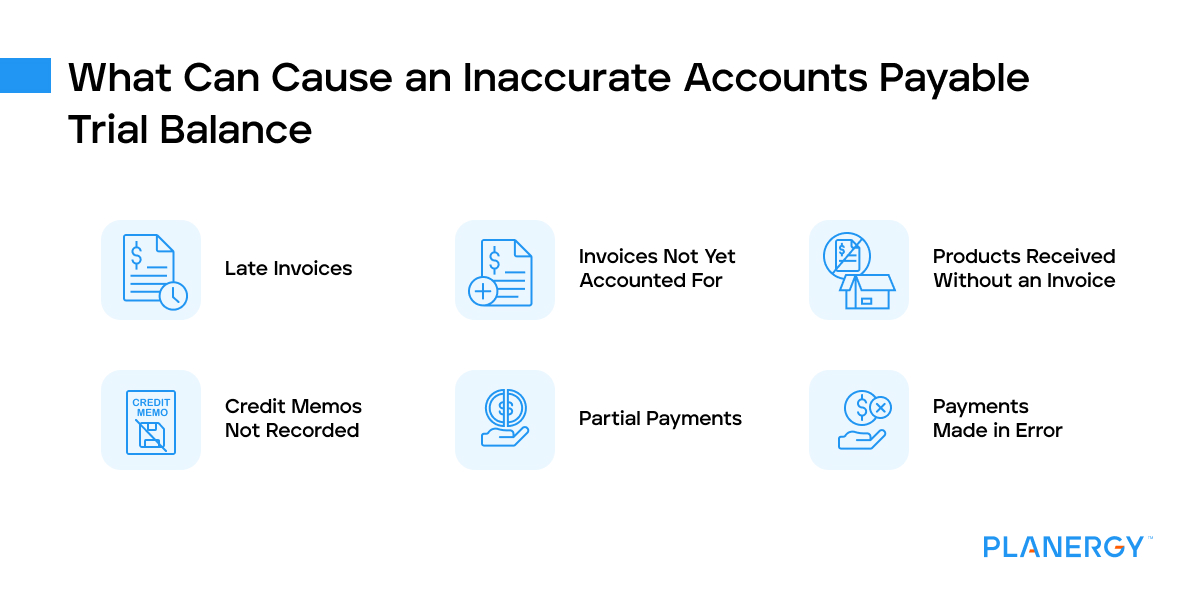

Let’s say you find an accounts payable invoice that has not yet been posted.

First, you’ll have to make a journal entry to record the AP invoice and the expense.

| Date | Account Name | Debit | Credit |

|---|

| 6-30-2023 | Postage Expense | $160 | |

| 6-30-2023 | Accounts Payable | | $160 |

Adjusted Trial Balance

The adjusted trial balance is run after making any adjusting entries.

After you record the above journal entry, you’re ready to run the adjusted trial balance for June 30, 2023.

Notice that the accounts payable and postage expense amounts are different.

| Account Number | Account Name | Debit | Credit |

|---|

| 1000 | Checking Account | $125,200 | |

| 1005 | Accounts Receivable | $27,000 | |

| 1020 | Inventory | $6,000 | |

| 2000 | Accounts Payable | | $15,610 |

| 2005 | Notes Payable | | $51,000 |

| 3000 | Stock | | $45,000 |

| 4000 | Revenue | | $57,000 |

| 5000 | Wages | $8,000 | |

| 5005 | Postage Expense | 1,660 | |

| 5020 | Insurance Expense | $750 | |

| | | | |

| | Totals | $168,610 | $168,610 |

Other common adjusting entries include deferred revenue, prepaid expenses, and depreciation expense.

Post-Closing Trial Balance

The post-closing trial balance is the final trial balance you’ll run after temporary accounts such as revenue and expense accounts have been closed for the accounting period.

Once this is complete, the post-closing trial balance will reflect beginning balances as of July 1, 2023.

| Account Number | Account Name | Debit | Credit |

|---|

| 1000 | Checking Account | $125,200 | |

| 1005 | Accounts Receivable | $27,000 | |

| 1020 | Inventory | $6,000 | |

| 2000 | Accounts Payable | | $15,610 |

| 2005 | Notes Payable | | $51,000 |

| 3000 | Stock | | $45,000 |

| 4000 | Retained Earnings | | $46,590 |

| | | | |

| | Totals | $158,200 | $158,200 |

You can see that the post-closing trial balance has removed all temporary expense accounts as well as the revenue account.

This is done by subtracting your expenses from your revenue, which becomes retained earnings.

It’s important to remember that all of the accounts in your general ledger will be included in your trial balance.