We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with Planergy.

If you’re using accrual accounting, sometimes known as a double-entry accounting system, you’ll need to understand debits and credits.

Two of the most important accounting terms you’ll come across, every transaction you record must have a debit and a credit entry of equal value. Accounts payable accruals are no different.

Before we examine whether accounts payable is a debit account or a credit account, we’ll first look at debits and credits, what they are, and how they impact vital business accounts like accounts payable, accounts receivable, and inventory.

What Are Debits and Credits?

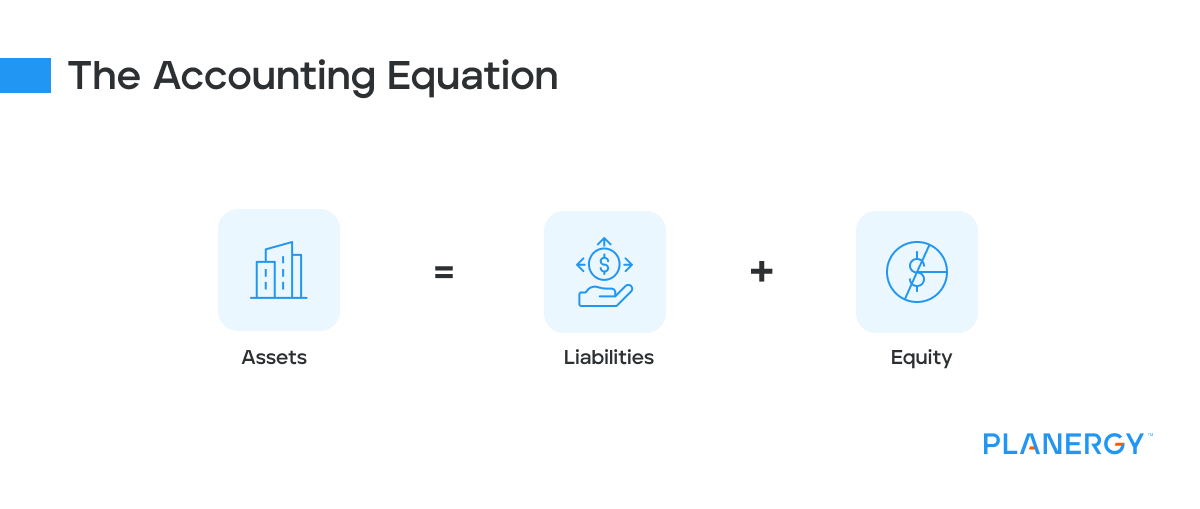

Debits and credits are used in accounting to ensure that you’re entering transactions using the accounting equation which is:

Assets = Liabilities + Equity

When you’re using accrual accounting every transaction should have a debit entry and a credit entry.

Debit totals are always on the left side of your accounting journal, while credit entries are on the right side of the journal.

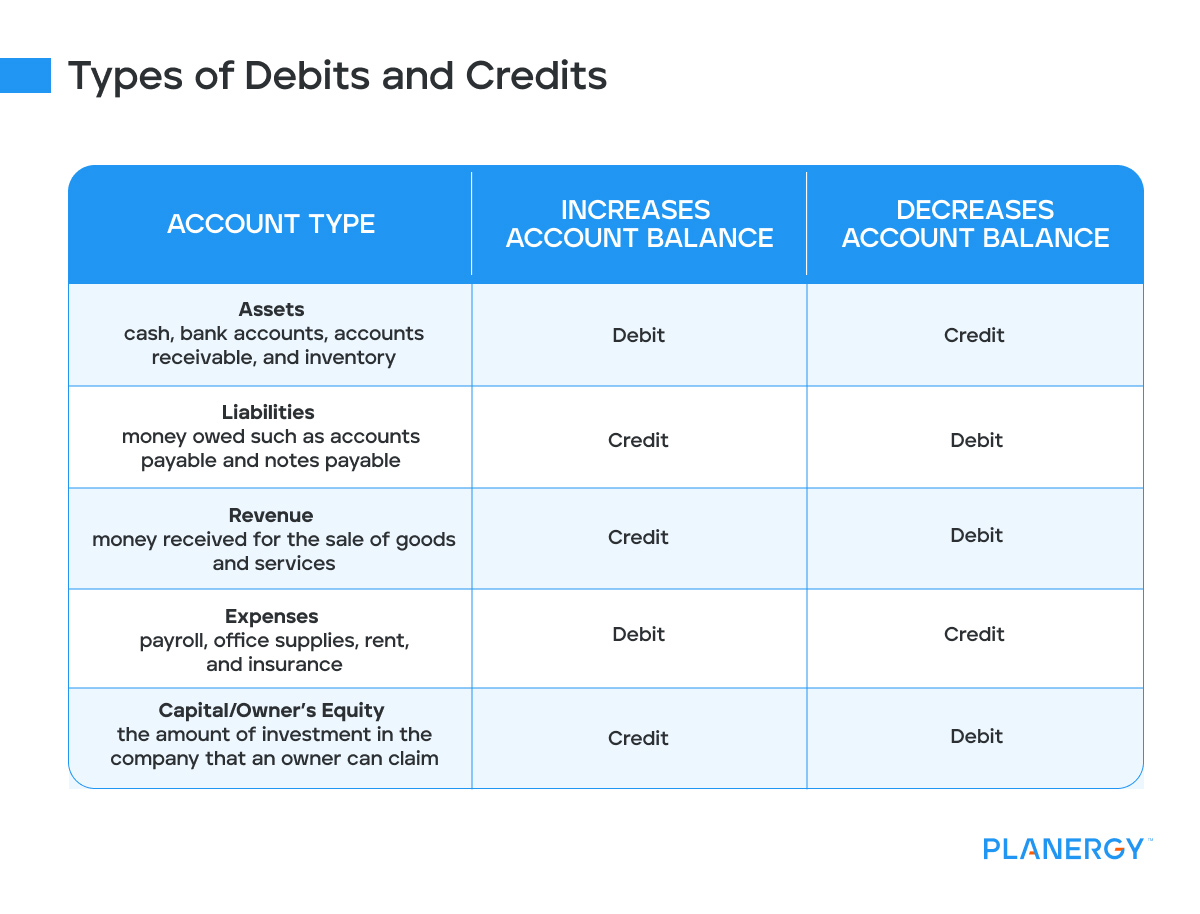

Depending on the type of account you set up in your chart of accounts, a debit may increase or decrease an account balance.

For instance, asset and expense account balances are increased when debited and decreased when credited, while liability, revenue, and owner’s equity account balances are increased when credited and decreased when debited.

Account Type

Increases Account Balance

Decreases Account Balance

Assets: cash, bank accounts, accounts receivable, and inventory

Debit

Credit

Liabilities: money owed such as accounts payable and notes payable

Credit

Debit

Revenue: money received for the sale of goods and services

Credit

Debit

Expenses: payroll, office supplies, rent, and insurance

Debit

Credit

Capital/Owner’s Equity: the amount of investment in the company that an owner can claim

Credit

Debit

Why Are Accounts Payable on the Credit Side?

Accounts payable represent money owed to vendors and suppliers, making it a current liability account.

Because of that, your accounts payable balance should always be a credit and recorded on the right side of the general ledger.

When those invoices are paid, the transaction is posted on the left side of the general ledger as a debit, reducing the account balance.

Is Accounts Payable Always a Credit?

Because you’re using accrual accounting, there must be a debit and a credit entry for any transaction, including accounts payable.

Your accounts payable balance should always have a credit balance in your general ledger.

A debit balance in your accounts payable account should be investigated since a debit balance usually occurs when an overpayment or duplicate payment has been made.

Accounts payable represents the amount of money that a business owes vendors and suppliers, while accounts receivable represents the amount of money that a business is owed from its customers.

Accounts payable is always a liability account on your company’s balance sheet, with accounts receivable a current asset on your balance sheet.

What Is the Difference Between Accounts Payable and Bills Payable?

Bills payable is the term used to refer to the actual invoice sent by vendors for payment. In most cases, bills payable is a direct reference to accounts payable, with the two terms used interchangeably.

Since most accounts payable transactions are accompanied by a bill, the bills payable total amount will usually match the accounts payable balance.

Bills payable, like accounts payable, are always recorded as a credit on your balance sheet, with the balance posted as a debit when paid.

What Are the Journal Entries Required When Processing Accounts Payables?

Two sets of journal entries need to be completed during the accounts payable process.

The first is recording the initial payable invoice to the appropriate expense account for the business purchases, with the second entry debiting accounts payable when the invoice is paid.

For example, Sam signed a contract on May 17, 2023, with ABC Marketing to create a marketing plan for his business. Sam receives the plan 12 days later along with an invoice for $1,500 dated May 31.

The marketing expense account is debited or increased with the above journal entry since expense account balances are increased when debited.

The accounts payable account balance is also increased because liability account balances are increased when credited.

If Sam had not received the above invoice until June 2, he would have to accrue the expense for May, since that’s when the expense occurred.

When Sam pays the bill in June, he’ll do the following journal entry:

Date

Account

Debit

Credit

5-31-2023

Accounts Payable

$1,500

5-31-2023

Cash

$1,500

This entry is done to reduce both the accounts payable balance and the available cash balance.

A debit entry to accounts payable reduces the balance of the account since it’s a liability, while a credit to the cash account also reduces the account balance because a credit to an asset account always reduces the account balance.

What Are the Journal Entries for Recording Debits and Credits in Other Accounts?

Understanding debits and credits and account types is essential for properly recording accounting transactions.

Let’s take a look at the journal entries you’ll need to make for each of the following account types.

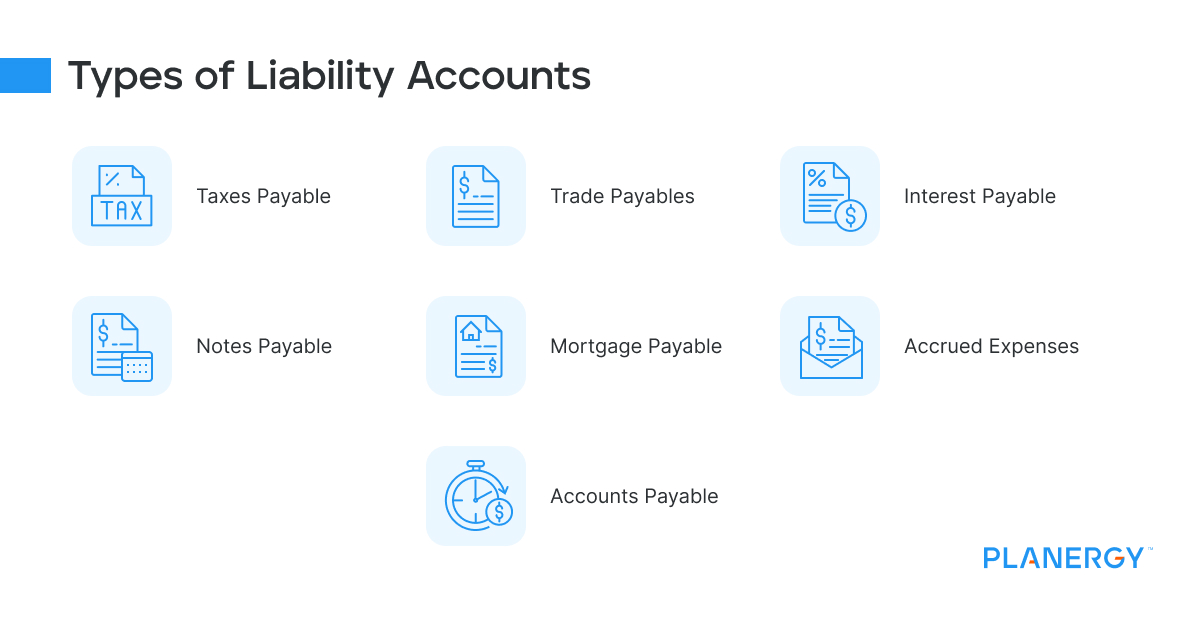

Liability Accounts

A journal entry to record an increase in a liability account is always a credit.

For example, to record additional invoices received for payment, you’ll always credit accounts payable and debit the appropriate expense.

Other liability accounts that need to be credited include:

Taxes Payable

Trade Payables

Interest Payable

Notes Payable

Mortgage Payable

Accrued Expenses

For any of the above accounts, to increase the balance of the account, you will need to credit it, debiting the account only when payment is made or an adjustment to the original invoice is required.

Owner’s Equity / Capital Accounts

If a business is privately owned, the owners will likely continue to invest money into the business. This type of investment is known as a capital investment and is often used for business expansion or to purchase equipment or add additional staff members.

For example, Will owns a small manufacturing company. With more orders coming in, he decides to add staff and update his equipment.

With revenue limited, Will decides to invest $100,000 of his own money in the business. Because owner’s equity or capital is an equity account, the journal entry that needs to be made to record Will’s investment will be as follows:

Date

Account

Debit

Credit

6-30-2023

Cash

$100,000

6-30-2023

Owner’s Equity

$100,000

This journal entry increases cash which is an asset as well as the owner’s equity account.

Along with capital investments, the balance in the owner’s equity account can change because of the following transactions:

Retained Earnings

Every time a business retains earnings in the business, the owner’s equity account balance increases or is credited.

Equity Withdrawals

Owners have the right to withdraw funds from the business for their personal use. When an owner withdraws money, the owner’s equity balance is reduced or debited.

Business Losses

Business losses can also reduce the owner’s equity account, with the owner’s equity debited for the amount of the loss.

For publicly traded companies, stock sales, dividends, and distributions can also impact the owner’s equity or capital account.

Accounts Receivable Accounts

Your company’s accounts receivable balance represents the amount of money due your company from customers that is still owed.

Since it is money owed to the business and not money the business owes, accounts receivable is an asset account.

The journal entry to record an accounts receivable transaction for services rendered is:

Date

Account

Debit

Credit

6-30-2023

Accounts Receivable

$5,000

6-30-2023

Accounting Services Sales

$5,000

Because services were provided to your customer on credit, you’ll enter the amount of the invoice as accounts receivable and increase sales by crediting the sales account, which is a revenue account.

When your customer pays the invoice, you’ll have to record the payment as follows:

Date

Account

Debit

Credit

6-30-2023

Cash

$5,000

6-30-2023

Accounts Receivable

$5,000

This transaction increases your cash, which is an asset account, and reduces the balance of your accounts receivable account since payment has been made.

Inventory accounts

Posting inventory transactions can be fairly straightforward for simple inventory purchases, but can become more complicated. To record a simple inventory transaction, you would complete the following journal entry:

Date

Account

Debit

Credit

6-30-2023

Inventory

$7,500

6-30-2023

Accounts Payable

$7,500

Since inventory is an asset, you will increase the amount of inventory by debiting the purchase and crediting accounts payable. If the purchase was made outright, you would credit cash instead of accounts payable.

Under the following circumstances, you’ll also need to enter adjustments to your inventory account to properly track the cost of goods sold:

Purchasing Raw Materials

This would be recorded as a debit to raw materials inventory and a credit to accounts payable because you’re increasing your inventory.

Adjusting Work-in-Progress Inventory

After the inventory is moved for product completion, you’ll need to debit (increase) the work-in-progress inventory account and credit (reduce) the raw materials account.

Product Completion

Once a product is complete, you’ll have to debit (increase) your finished goods inventory account and credit (reduce) the work-in-progress account.

Small business owners will be relieved to know accounting automation can complete many of these transactions for you, including data entry and inventory management.

The key to managing critical accounting tasks such as accounts payable is to first understand debits and credits and how each impact your accounts.

1. Use Planergy to manage purchasing and accounts payable

We’ve helped save billions of dollars for our clients through better spend management, process automation in purchasing and finance, and reducing financial risks. To discover how we can help grow your business:

Visit our Accounts Payable Automation Software page to see how Planergy can automate your AP process reducing you the hours of manual processing, stoping erroneous payments, and driving value across your organization.

2. Download our guide “Preparing Your AP Department For The Future”

Download a free copy of our guide to future proofing your accounts payable department. You’ll also be subscribed to our email newsletter and notified about new articles or if have something interesting to share.

3. Learn best practices for purchasing, finance, and more

Browse hundreds of articles, containing an amazing number of useful tools, techniques, and best practices. Many readers tell us they would have paid consultants for the advice in these articles.

Stay up-to-date with news sent straight to your inbox

Sign up with your email to

receive updates from our blog

This website uses cookies

We use cookies to personalise content and ads, to provide social media features and to analyse our traffic. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that you’ve provided to them or that they’ve collected from your use of their services.