Ironically, best practices for year-end accounting should start at the beginning of the year, since many of the issues that present themselves at year-end are a result of issues incurred earlier in the year that only come to light during the year-end closing process.

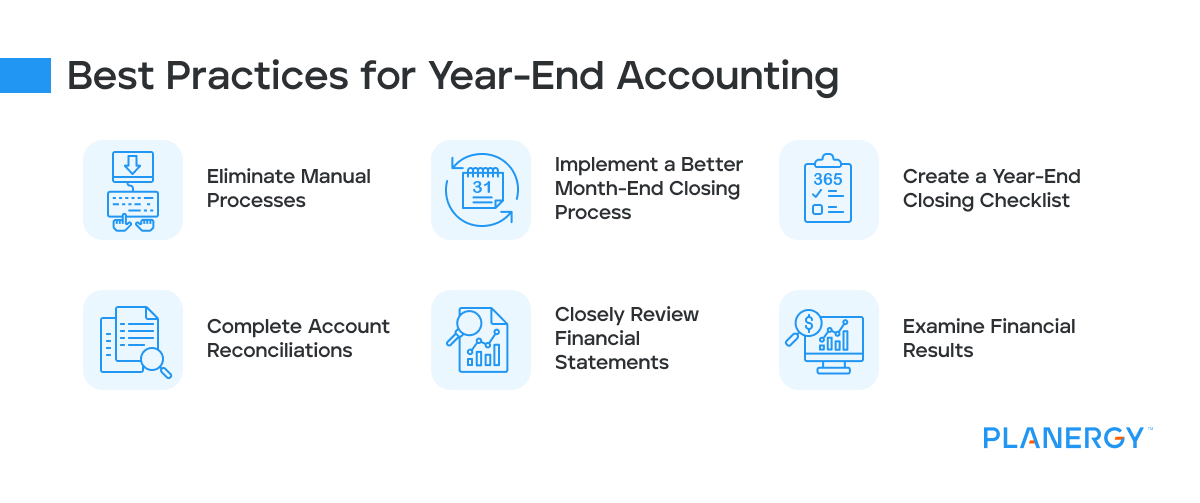

Eliminate Manual Processes

One of the best ways to streamline the year-end closing process is to eliminate manual processes and switch to an automated accounting application.

This one change can trim significant time off both month-end and year-end closing. An automated system can also increase accuracy, eliminate the need to manually match documents, and can significantly reduce stress for your accounting team.

Implement a Better Month-End Closing Process

If your month-end closing process is sound, chances are that your year-end closing will be relatively quick and painless.

When a solid month-end (or quarter-end closing for smaller businesses) is in place, any issues that arise can be promptly addressed, eliminating any surprises down the road.

Like year-end closing, a good month-end closing process should include a review of all account balances and making any necessary adjustments at the time the issue is identified so that they don’t show up at the end of the year.

Create a Year-End Closing Checklist

Having a checklist in place helps keep you on track and ensures that nothing of importance is overlooked. We’ll have more on what a checklist is and what should be on the checklist shortly.

Complete Account Reconciliations

Year-end is the best time to review your accounts payable and accounts receivable financial transactions for both accuracy and collectability.

For AR balances, this may include an assessment of prior collection attempts and whether the balance is worth leaving on the books or if it should be written off as bad debt.

Reviewing AP accounts is just as important, making sure that unpaid balances are accurate and that all invoices for outstanding balances have been received. This also allows you to follow up with vendors if an invoice is missing.

Closely Review Financial Statements

Once all adjusting entries have been completed, the CFO or finance department manager will want to spend time reviewing current year-end totals against previous year totals for potential red flags.

Carrying out vertical analysis of the balance sheet and horizontal analysis of the balance sheet can identify issues for further investigation.

For example, if your rent expense was $12,000 for 2021 and $45,000 for 2022, and you’re in the same building, the account will need to be reviewed to determine why the two totals are so different.

Examine Financial Results

Once adjustments have been made, it’s a great time to analyze your financial results using accounting ratios. When calculated regularly, these ratios can help identify business trends and assist when making business decisions.